Tech buyers relocating from San Francisco to New York in 2026 are concentrating on new construction, full-service condo neighborhoods. In Manhattan, that means NoMad, Flatiron, Chelsea, Gramercy, and Tribeca. In Brooklyn, it means Williamsburg and DUMBO.

They pick those areas for proximity to the offices clustering in Hudson Square, SoHo, and Midtown South, and for the turnkey, amenity-rich buildings this buyer tends to want. But the three things that actually decide whether the move goes well are the ones nobody tells you on the way in. New York is not a tax escape from California. The building matters more than the apartment. And the process has far more gray area than any calculator or listing photo suggests.

I represent these buyers. I helped a tech founder couple into a Gramercy penthouse, and I work with engineers, operators, and executives across the industry. This is the honest version of what I tell them.

A quick note on who this is for. People hear “AI wealth” and assume it means a handful of founders at frontier labs. The real audience is much wider. It is engineers, product leaders, finance and legal professionals, and executives across tech, with the AI boom acting as the catalyst that is pulling talent and money toward New York right now. If you work in tech and you are thinking about a move, this is written for you.

Why are tech and AI people moving from San Francisco to New York in 2026?

For most of the last decade, tech wealth was a Bay Area story. That is changing, because the companies came east. Anthropic is closing in on a lease for an entire building of roughly 466,000 square feet at 330 Hudson Street in Hudson Square, which is a full building commitment rather than a satellite office. OpenAI expanded around the Puck Building in SoHo. AI was a dominant share of a record tech leasing quarter in Manhattan in early 2026, and New York is now home to more than 9 percent of all AI workers in the country, ahead of Seattle, Boston, and Los Angeles. New York has also been leading the U.S. in net gains of relocating tech workers, and a meaningful share of those people are coming straight from San Francisco.

When a company leases a whole building, it is moving senior people. Those are the directors, staff engineers, and executives who buy rather than rent. So the migration you may have heard about anecdotally is real and measurable. The honest caveat is that it is arriving steadily, not in one overnight wave. I will come back to the IPO timing question, because most of the coverage gets it wrong.

Where should you live based on where you work?

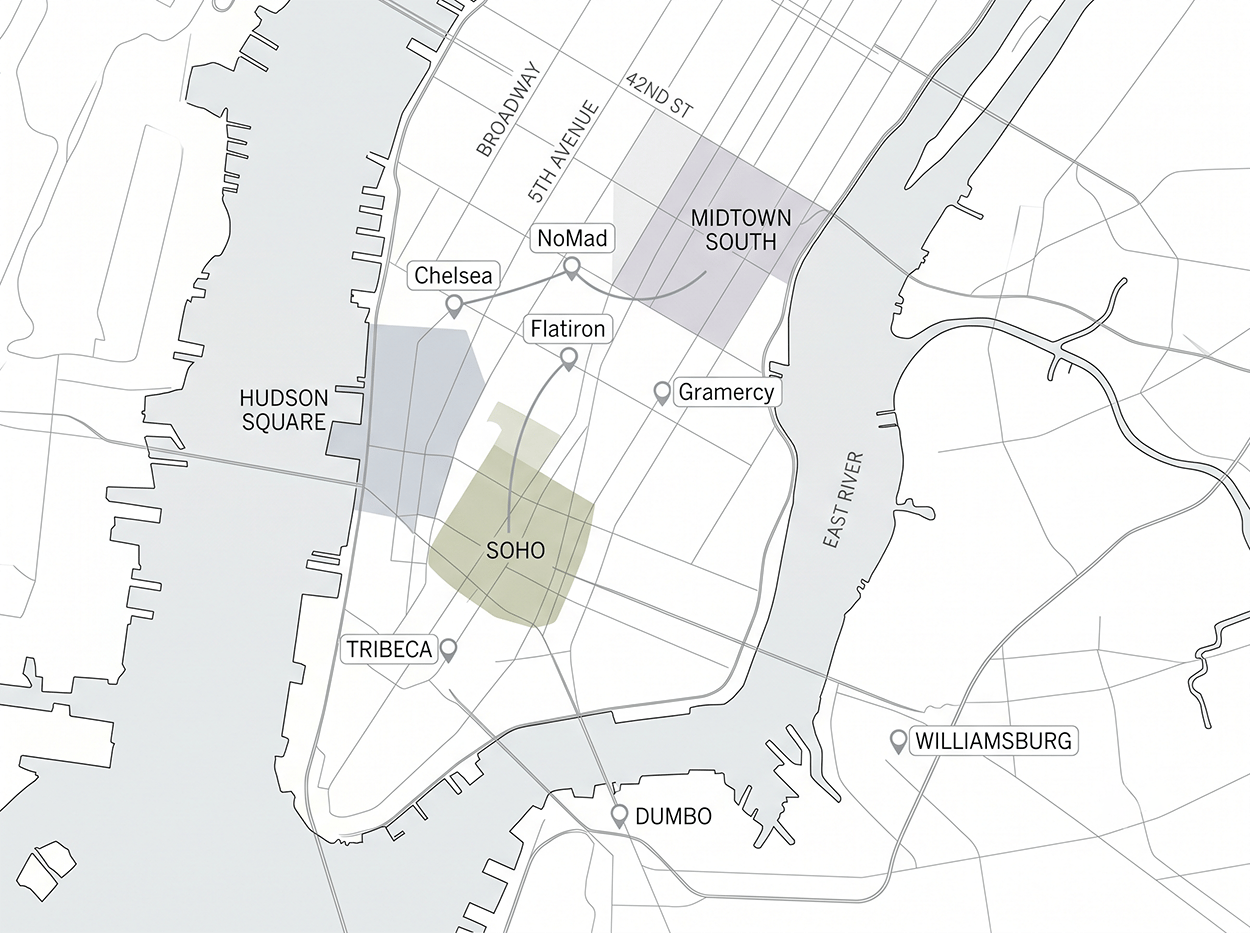

The single most useful filter for someone coming from San Francisco is your commute. New York rewards living close. A short subway ride or a walk beats any car commute you had in California. Here is how the office map translates into neighborhoods.

|

If your office is in... |

Strongest neighborhoods |

Why it works |

|

Hudson Square or SoHo (Anthropic, OpenAI, Google's NYC campus) |

Tribeca, West Village, Hudson Square, DUMBO, Williamsburg |

Walkable or one short train ride, new construction with full service, downtown energy |

|

Midtown or Flatiron (many tech and VC offices) |

NoMad, Flatiron, Chelsea, Gramercy |

Central, design-forward full-service towers, quick commute in every direction |

|

Flexible or hybrid |

Williamsburg, DUMBO, Chelsea |

New construction, outdoor space, water views, shorter commute than the suburbs |

NoMad and Flatiron have become magnets for branded new development, the kind of buildings with hotel-grade service that match the turnkey lifestyle this buyer wants. Tribeca offers branded new construction and large floor plates for buyers comfortable with above three million dollars. Across the river, Williamsburg and DUMBO suit a younger tech buyer who wants new construction, light, and water views with a genuinely short commute into the downtown office corridor.

Is New York actually a tax escape from California?

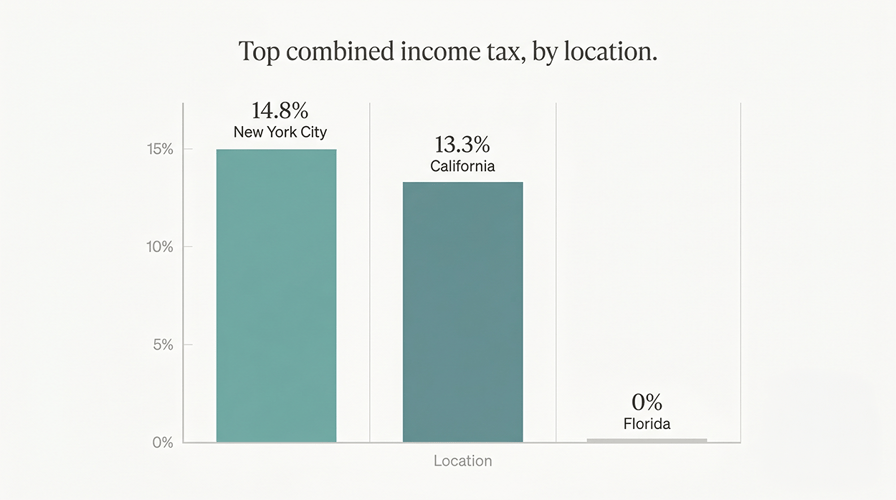

No, and this is the most important myth to puncture before you relocate, because I watch people get it wrong.

California's top marginal income tax rate is 13.3 percent. New York State's top rate is 10.9%, but New York City adds its own resident income tax of up to roughly 3.9% on top of that, which pushes a top bracket city resident to a combined state and city rate near 14.8%. That is higher than California. If your main motivation is escaping income tax, New York is not the answer, and you should know that going in. The people who relocate purely for tax reasons tend to choose Florida, which is why Miami is the other big destination for this money.

So why move here? For the city, the career, the density of talent and capital, and the life. Not the tax bill. Being clear-eyed about that prevents an expensive misunderstanding.

Where New York does offer real opportunity for tech wealth is on the asset side, not residency. One of my clients, an engineer whose company went public, was staring at a large tax bill on his windfall. Instead of parking everything in a single home, he used the short-term rental and bonus depreciation strategy on an investment property to offset a meaningful chunk of that bill, then bought a cash-flowing rental in Williamsburg with me. He is now several properties in. That short-term rental strategy generally requires property outside New York City, because the city's Local Law 18 effectively bans rentals under 30 days, and it is highly specific to each person's situation, so it is absolutely a conversation for your CPA. The point is not the tactic. It is that the smartest buyers treat a windfall as capital to deploy and diversify, not just a budget for a trophy apartment.

|

A quick boundary. I am a licensed real estate broker, not a CPA or an attorney. Nothing here is tax or legal advice, and the strategies above depend entirely on your situation. Work through your residency, tax, and ownership questions with qualified professionals before you move or buy. I am happy to introduce you to specialists who do this for tech clients. |

Why two "identical" apartments are not the same investment

This is the thing I most wish relocating buyers understood. Real estate is not cut and dry. There is a lot of gray in the middle, and no matter how simple anyone makes the process sound, there are hurdles you have not considered yet. Two apartments side by side in the same building, same line, same finishes, will not necessarily trade the same or appreciate the same. The unit seduces you. The building decides the outcome.

What actually drives value and risk sits below the surface. The building's financials and reserve fund. The sponsor's track record. The amenity-to-unit ratio, which governs whether your common charges stay stable over time. The board and the bylaws. The days on market patterns for that specific building. And how the price per square foot, including outdoor space, compares to true value. Most agents price outdoor space badly, which is its own opportunity. This is the whole reason we built the Undivided Value Index, and it is the work that separates a good-looking purchase from a good one. When you are coming from out of town and buying into new construction, you cannot see any of this from the listing.

A real example: a tech founder couple in Gramercy

A newly married tech founder couple who had just moved to New York came to me for their first home. They started with a modest budget and a clear wish list. Downtown, especially SoHo. Walkable. New construction only. Outdoor space. A flexible layout for a home office. Room to entertain. After touring resale units, they pivoted decisively toward new development, and then toward penthouses with skyline views.

We landed on a full-floor penthouse at Celeste Gramercy, with 2,722 interior square feet plus a 935 sqft private terrace, designed by Eran Chen of ODA Architecture. One bedroom became a multifunctional office, Zoom room, and guest room with a Murphy bed. The rooftop terrace had an entertaining lounge, a dining area, and a full outdoor kitchen.

But the home is not the lesson. The analysis is. We ran three years of penthouse comps in Gramercy, a price per square foot model for both interior and exterior space, and proprietary scatter plot modeling to establish fair value, precisely because outdoor space is so often mispriced. We reviewed build quality on site and stress tested the amenity-to-unit ratio to confirm the common charges would stay stable. The market favored buyers at the time, which gave us leverage. The result was 950,000 dollars off the asking price and more than 150,000 dollars saved in closing costs, which came to over a million dollars in total, roughly 13 percent below market for a penthouse of that type. It has since appreciated by about 11 percent.

That outcome did not come from finding the apartment. It came from understanding the building, the comps, and the moment, and from knowing how to negotiate the gray.

How is buying in NYC different from buying in San Francisco?

Several ways, and they trip up nearly every transplant.

First, condos versus co-ops. Roughly two-thirds of Manhattan's apartment stock is co-ops, which are run by boards that can reject buyers, scrutinize finances in detail, restrict LLC and pied-a-terre ownership, and limit financing. For a buyer whose wealth is concentrated in company stock rather than a long salary history, co-ops are often impractical. Condos allow LLC ownership, accommodate non-traditional income and asset profiles, and close on a predictable timeline. For most relocating tech buyers, condos are the path. Just treat it as a fit question for your situation, not a blanket rule.

Second, closing costs are higher and structured differently than in California. New York buyers face a few things California buyers do not. There is the NYC mansion tax, a progressive tax on purchases of a million dollars or more that runs from 1 percent up to 3.9 percent at the highest tiers. There is the mortgage recording tax, roughly 1.8 to 1.925 percent of the loan amount on financed purchases. On new development specifically, buyers are often asked to pay the sponsor's transfer taxes and attorney fees, which can add another 2 percent or more, and which are negotiable, so this is a place where representation pays for itself. And the whole process is attorney-driven. New York deals run through real estate attorneys, whereas California's run through escrow and title. You will need one, and we coordinate it.

Third, and this one is underrated, personalities are part of the deal. A New York transaction involves sponsors, listing agents, attorneys on both sides, building management, and sometimes a board, each with their own incentives and temperament. A lot of getting a deal done well is managing those personalities and the friction between them. None of that is in a calculator, and it is a big part of what you are actually hiring for.

What is the smartest way to time a purchase around an IPO or liquidity event?

Do not market your move to the IPO date, and do not wait for it either. Here is the part most coverage gets wrong. The 2026 AI IPOs are not instant cash-out events for employees. SpaceX's offering, for example, is structured as all primary, which means the proceeds fund the company rather than selling shareholders, and insiders face a 366-day lockup. OpenAI's and Anthropic's IPO proceeds also unlock fully only after lockup periods expire, generally around six months after listing, which points to a larger liquidity wave in 2027.

The money that is actually spendable right now is the quieter kind. Secondary sales and employee tender offers have been putting cash in people's hands well ahead of any public listing. Buyers who move during this current window are also transacting against today's softer financed segment prices, before the larger post-lockup wave arrives. And you do not always have to sell stock to buy. Pledged asset lines let qualified buyers borrow against a portfolio to fund a purchase without triggering a taxable sale, with real risks to weigh. We cover that in detail in our pre-IPO playbook.

The bottom line

The migration from San Francisco to New York is real, it is tied to where the companies are physically building, and it is arriving steadily rather than all at once. The buyers who do well pick a neighborhood by commute, buy new construction full-service condos structured for flexible ownership, budget the true all-in cost, and stay honest with themselves that New York is a lifestyle and career move, not a tax play. They also remember that the building, and the gray, human work of getting a deal done, matters more than the apartment.

If you are relocating from the Bay Area or advising someone who is, the right time to understand your options is before the move, not during it.

Book a 30-minute strategy call. No pitch. Just the analysis.

Undivided Inc. is a licensed real estate brokerage. No financial, tax, or legal advice is provided in this article. Information is general and may not reflect your specific circumstances or the latest rules, so consult qualified professionals before acting.