You found the perfect condo. You're ready to make an offer. Then your broker asks: "Have you sold your current place yet?"

That's when the math stops working.

Most condo owners in Manhattan assume that selling and buying simultaneously is straightforward. List your place, find the next one, coordinate the closings. Done.

Except NYC condo transactions rarely align that cleanly.

I've walked six clients through this process in the past two weeks alone. Same building, same question: "How do we buy the next place if we still own this one?"

Here's what actually happens, and the four structures that work when the timing doesn't.

The Equity Trap

Let's use real numbers.

You own a $1.2M condo in Chelsea. Your mortgage balance is $700K. You want to buy an $1.8M place in the West Village.

You need $360K for the 20% down payment. Right now, that money is locked in your current condo as equity, the $500K gap between what it's worth and what you owe.

The plan seems obvious: sell your condo, extract the equity, and use it for the new down payment.

But here's where it falls apart.

Your sale closes June 15th. The seller of your new condo needs to close by June 8th. One week gap. You can't buy the new place until the proceeds from your sale hit your account. Which means you either:

- Ask the seller to delay (they'll likely refuse)

- Source $360K another way (bridge loan, HELOC, family)

- Walk away from the purchase

This is the moment most buyers panic.

The Contingency Problem

The alternative: make an offer before you've sold.

You write a contingent offer: "I'll buy your condo, but only if mine sells first."

In theory, this protects you. In practice, contingent offers get rejected 73% of the time in competitive Manhattan buildings.

Why? Because another buyer will submit a clean offer without conditions. The seller picks certainty every time.

So you found the perfect place, but you can't compete for it because you haven't sold yet.

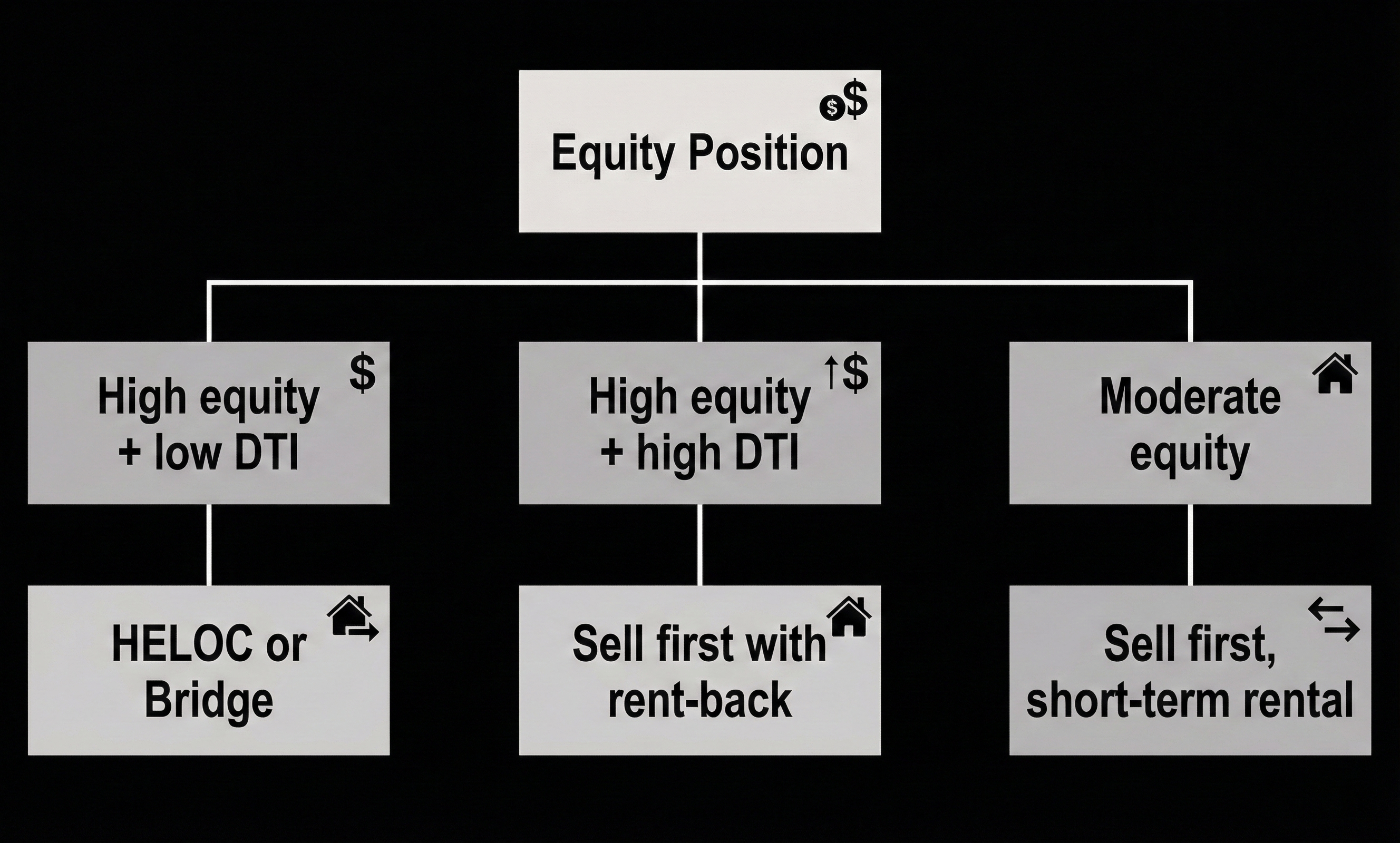

Four Structures That Actually Work

The right approach depends on your leverage position, not your preference.

Option 1: Sell First, Negotiate a Rent-Back

You close on your sale, collect proceeds, then rent your own apartment back from the buyer for 30-60 days while you close on your purchase.

The catch: About 40% of NYC buyers reject rent-backs outright. When they accept, you're paying market-rate rent ($5K-$8K/month for a two-bedroom) plus security deposit.

Who this works for: Sellers in buildings where demand gives them leverage to dictate terms.

Option 2: Access Equity via HELOC

You take out a home equity line of credit against your current condo. Use it for your new down payment. Repay when your sale closes.

The catch: HELOCs count toward your debt-to-income ratio. If your current mortgage already represents 28% of your gross income, and the new mortgage would add another 25%, you're at 53% DTI before the HELOC. Most lenders cap DTI at 43-50%, which disqualifies you.

Who this works for: Buyers with low existing DTI who can absorb the additional payment in their qualification.

Option 3: Bridge Financing

A short-term loan covering the gap between your old mortgage payoff and your new down payment.

The numbers: 8-12% APR with 2-3 points upfront. On a $200K gap, that's $4K-$6K in origination fees plus $1,300-$2,000/month in interest. If your sale takes 90 days, you're looking at $8K-$12K total.

Who this works for: High-income buyers with substantial equity who need timing certainty and can absorb the cost.

Option 4: Sell First, Preserve Optionality

Close your sale, bank the proceeds, move into a short-term rental, and buy when the right property appears, without contingency pressure.

The trade-off: You move twice. Storage runs $200-$600/month. Short-term rentals are expensive and scarce in NYC. But your purchase offer is clean, which matters in competitive buildings.

Who this works for: Buyers who value negotiating position over convenience.

What Most Agents Miss

The structure matters less than the math.

Before you list, you need three numbers:

- Your actual equity position (current value minus mortgage balance)

- Your DTI with and without your current mortgage (determines if you can qualify for two loans simultaneously)

- Your liquid cash position (for down payment, closing costs, and backup plans)

Because here's what happens when you skip this step:

You sell your condo. You find your next place. You realize you're $50K short because closing costs ran higher than expected. Now you're scrambling to borrow from family, delay the closing, or lose the deal.

Or: You make a contingent offer. It gets rejected. You realize too late that contingencies don't work in your price range. You wasted three weeks.

The stress isn't the dual transactions. It's the improvisation.

The Current Market Context

Manhattan condo absorption slowed 18% in Q4 2024. Inventory in certain corridors is tightening while others are softening.

Translation: if you're moving up this year, you could be selling into weakness while buying into strength. Which means you'll net less on the sale and potentially pay more on the purchase.

That imbalance needs to inform your structure. Maybe you price aggressively on the sale to create certainty, then lean into negotiation on the buy side where you have time and liquidity.

The Bottom Line

Condo owners moving within Manhattan face a coordination problem disguised as a timing problem.

The real question isn't "Can we time both closings perfectly?"

It's: "How do we structure this so we're not making compromised decisions on either side?"

The right structure removes 80% of the anxiety. The wrong one creates pressure decisions that cost real money.

If you're considering a move this year, or know someone who is, the planning starts before the listing.

Feel free to reach out if you want to walk through the math for your specific situation. Even if you're a year out, knowing your leverage position now shapes better decisions later.

Ready to Get Started?

Here's what you'll get:

✓ Curated Listings

We handpick properties that fit you, saving you time by showing homes that match what you want.

✓ Luxury Amenities

We highlight top-tier amenities so your new home delivers the prestige and quality you expect.

✓ Market insights

We provide detailed market comps and insights to guide your decision-making with confidence and clarity.